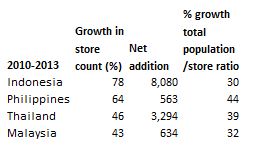

There has been a significant increase in the number of convenience stores/minimarts (C&M) opened between 2010 and 2013 in Malaysia, Indonesia, the Philippines and Thailand with Indonesia leading in terms of the net addition of stores and growth in store count, up respectively by 8,080 outlets and 78%. The Philippines ranked second in store count growth, while Thailand ranked second in the net addition of new outlets.

|

| Population and urban/rural split data from World Urbanization Prospects, The 2009 Revision, Population Division, UN, store data from annual reports. Note: not all convenience store and minimarts are included. Indonesia excludes Circle K, totaling 415 as of 31 March 2013. Malaysia comprises KK Mart, 99 Speedmart and 7-Eleven. Thailand’s number excludes 108 Stores (2012: 630 outlets), Tops Daily (2012: 130 outlets) and CP Fresh Mart (2012: 720 outlets). Compiled by Tan Heng Hong |

The consequence of the expansion of the C&M sector is the narrowing of the total population/store ratio. Even at 6,564 people/store in Thailand, the number of C&M is expected to rise as 7-Eleven, FamilyMart, Tesco and Big C expand their store network, driven by 7-Eleven. 7-Eleven aims to have 10,000 stores by 2017, an increase from 7,429 in 2013.

|

|

In Indonesia, growth is fuelled by the two leading minimarts – Indomaret and Alfamart, in the Philippines by 7-Eleven and in Malaysia by 99 Speedmart and 7-Eleven.

The Philippines appears to be the bright spot. The density of C&M is low compared to the three neighbouring countries due in part by the strength of the ubiquitous sari-sari stores (mom-and-pop grocery stores). The same situation can be said of Indonesia where the traditional trade channel is dominated by toko and warung. If Indonesia can achieve a ratio of one store for 12,635 people in a country dominated by toko and warung, the same can potentially happen to the Philippines. Both countries have a similar GDP per capita.

|

| From Deloitte citing Oxford Economics data |

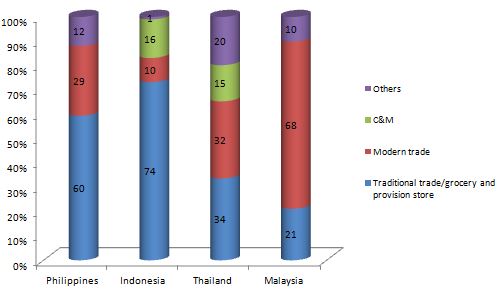

According to Kantar Worldpanel data, the share of traditional trade & grocery and provision store in household FMCG spending also the highest Indonesia at 74% and in the Philippines at 60% of which sari-sari accounts for 46%. In Thailand, despite the share of convenience store has risen to 15% at the expense of the modern trade and the traditional channel. In Indonesia, minimarket has craved a niche for itself accounting for 16% of total household FMCG spending, higher than the 10% spent in the modern trade.

|

|

In the Philippines, what is missing is a store format, minimart, that bridges convenience store and supermarket. The minimarket has the potential to account for an increasing share of household FMCG spending that would otherwise go into the modern trade (supermarket) and traditional trade (sari-sari). The key to the success of minimart in the Philippines is to ensure the price is not higher than convenience store but the price can still be slightly higher than supermarket to compensate for the convenience provided. The main role of the minimarket is to serve as a neighbourhood store offering a wide variety of popular goods at competitive prices.

The entry of Alfamart into the Philippines is significant because the minimarket format can potentially fill a gap in the market. Even through the Alfamart store in the Philippines is called a convenience store, it should compete with both convenience stores and sari-sari outlets, depending on their location.

What’s next

The growth of the call centre/BPO industry in the Philippines has been the driving force of the convenience store sector with employment in the call centre sector rising to 0.9mn in 2013 from 0.24mn in 2006. The rising middle class is also a catalyst of the growth of the convenience store sector. However, a faster rate of store expansion can be achieved if the C&M format can compete successfully with the sari-sari stores. Based on the experience of the Indonesian minimarket model, minimarket may fuel the next leg of growth for the C&M market in the Philippines.

|

|

{kind=link}